Why I am still a bear – Part 2

Sorry for delay in continuing this series. It has been a long week, but let’s get to it for today!

Reason #2: Earnings matter: Price/Earnings ratios mean revert over long periods of time, whether there is Fed intervention or not

There is this funny premise that some of us old guys adhere to regarding the stock market: a stock’s earnings (now and future) should be the primary basis of value. That may seem logical, but many investors don’t think of stocks that way. They think stocks are more like “sophisticated gambling”…of course, many think it is a can’t lose game. But I digress…

Don’t be mean

As much as my kids are saints, there are times when they argue continuously. I get it. It’s hard to have a roommate called your brother, but at the end of the day, as a parent you implore them to resolve it and “DON’T BE MEAN”.

Well, the world of stocks, we have have different kind of mean. It’s called the reversion to the mean. Statistically, it means that over time what ever statistic you value tends to “revert” to its historical average. In the case of earnings for stocks, we have been ahead of or significantly “over” the average for quite some time, so a reversion means that earnings should be headed down. If earnings were below the mean, then we should expect them to rise.

First, know that earnings last year on the S&P 500 were lower than in 2018, so they were already trending lower before the crisis.

Second, as we discussed last week, most “experts” and Wall Street prognosticators believe that “This Time Is Different”. Basically, the belief is that we are smarter, more sophisticated investors and that companies are better now than in the past so they should be permanently valued “HIGHER” than in the past. Oh…and then there’s the Fed. We will talk about that in a minute.

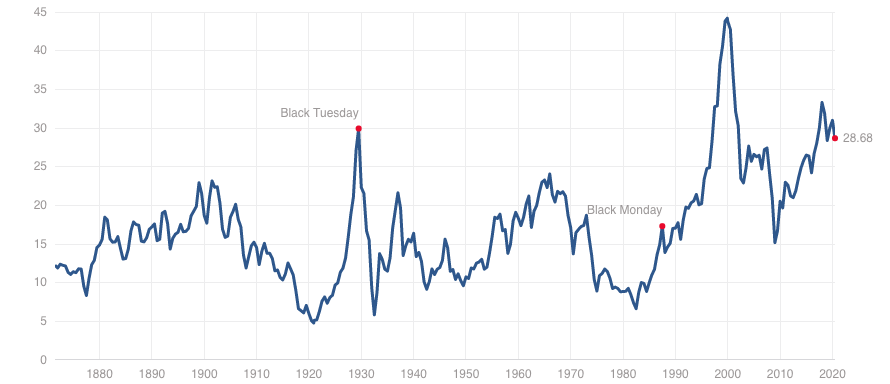

Below is an historical chart of the Shiller P/E ratio as far back as data goes. The historical “Mean” or “Average” is 16.72. Today, the ratio is 28 and climbing. In fact, once we get updated earnings for this past quarter, my guess is that the ratio will spike to an all time high.

But let’s take a quick detour…the Federal Reserve bank was created in 1913 and since that time has forced its policy upon the US financial system. In the beginning of the Great Depression, they were slow to adopt easy monetary policy and then during what looked like recovery, they were quick to raise rates. They also led us through the hyperinflation days of the 1970s (which seemed never-ending), and then eased interest rates starting in 1982 basically until now. Their actions and policies have resulted in numerous boom and bust cycles since their inception. In recent history – 2000 was no exception. 2008 no exception. 2020 will be no exception.

There is an underlying theme on Wall Street today that “fighting the Fed” is a losing proposition. Unfortunately, rolling with the Fed results in all the booms and busts. Maybe the highs and lows are exacerbated by the Fed’s actions, and maybe not. I am not an economist.

From what I can tell, regardless of Fed actions, the earnings of companies and the prices you pay for those earnings matter. Look at the peaks in the chart above. That is paying a high price for the earnings received. This gets back to one of the basics of stocks – buy low, sell high.

In today’s environment, the P/E ratio is extremely high and historically, it is due to revert back to its average. A closer look at that chart above will tell you that over the past 27 years, we have had only one year when the Shiller P/E ratio was at its average (2009). One year.

Some additional insight on what’s to come:

The earnings decline will be greater than expected, and this will only cause the P/E ratio to spike significantly higher (and as I commented above…potentially to all time highs). As it stands, Wall Street currently only expects a quick 20% decline in earnings…even though over 1/2 of the S&P 500 companies have pulled “guidance” for at least the 2nd quarter. That basically means that companies don’t know what their business is going to look like or how much they will sell/earn. It is hard to project when COVID-19 brought so much to an immediate halt!

With the great earnings unknown ahead, be prepared for record P/E ratios and what is to follow…a reversion to the mean.

Thanks for listening…tomorrow will be fun as we look at managing money compared to trading stocks. They are very different beasts!

God bless,

Josh